Data Science Portfolio

House Prices: Advanced Regression Techniques

Introduction

This project is for the Kaggle competition House Prices: Advanced Regression Techniques. The dataset can be found on the competition page here:

https://www.kaggle.com/c/house-prices-advanced-regression-techniques/overview

The data consists of 81 total variables, many of which are redundant and/or unnecessary. Our target variable which we are trying to predict is SalePrice.

We will first examine our features through visualizations, and then do feature engineering. Finally, we will do three iterations of model building:

1) Simple feature selection based on manual inspection

2) Feature importances from random forest regression

3) Principal Components Analysis

Preparing the Data

Loading the Data

import sys

import time

import numpy as np

import pandas as pd

import scipy

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.svm import SVC

from sklearn import ensemble

from sklearn import linear_model

from sklearn import neighbors

from sklearn.linear_model import LinearRegression

from sklearn.linear_model import Ridge

from sklearn.linear_model import Lasso

from sklearn.ensemble import RandomForestRegressor

from sklearn.ensemble import RandomForestClassifier

from sklearn.model_selection import cross_val_score

from sklearn.feature_selection import SelectKBest, f_classif

from matplotlib.mlab import PCA as mlabPCA

from sklearn.preprocessing import StandardScaler

from sklearn.preprocessing import LabelEncoder

from sklearn.decomposition import PCA

from sklearn.model_selection import train_test_split

from sklearn.metrics import precision_recall_curve

from sklearn.metrics import average_precision_score

from sklearn.metrics import classification_report

from sklearn.metrics import mean_squared_error

from sklearn.impute import SimpleImputer

from sklearn.model_selection import GridSearchCV

from sklearn.pipeline import Pipeline

import statsmodels.formula.api as smf

from scipy import stats

from scipy.stats import normaltest

from scipy.special import boxcox1p

from scipy.stats import norm

from scipy.stats import skew

%matplotlib inline

np.set_printoptions(threshold=sys.maxsize)

pd.set_option("display.max_rows", 100)

df_train = pd.read_csv('train.csv')

df_train.head()

| Id | MSSubClass | MSZoning | LotFrontage | LotArea | Street | Alley | LotShape | LandContour | Utilities | ... | PoolArea | PoolQC | Fence | MiscFeature | MiscVal | MoSold | YrSold | SaleType | SaleCondition | SalePrice | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 60 | RL | 65.0 | 8450 | Pave | NaN | Reg | Lvl | AllPub | ... | 0 | NaN | NaN | NaN | 0 | 2 | 2008 | WD | Normal | 208500 |

| 1 | 2 | 20 | RL | 80.0 | 9600 | Pave | NaN | Reg | Lvl | AllPub | ... | 0 | NaN | NaN | NaN | 0 | 5 | 2007 | WD | Normal | 181500 |

| 2 | 3 | 60 | RL | 68.0 | 11250 | Pave | NaN | IR1 | Lvl | AllPub | ... | 0 | NaN | NaN | NaN | 0 | 9 | 2008 | WD | Normal | 223500 |

| 3 | 4 | 70 | RL | 60.0 | 9550 | Pave | NaN | IR1 | Lvl | AllPub | ... | 0 | NaN | NaN | NaN | 0 | 2 | 2006 | WD | Abnorml | 140000 |

| 4 | 5 | 60 | RL | 84.0 | 14260 | Pave | NaN | IR1 | Lvl | AllPub | ... | 0 | NaN | NaN | NaN | 0 | 12 | 2008 | WD | Normal | 250000 |

5 rows × 81 columns

df_train.describe()

| Id | MSSubClass | LotFrontage | LotArea | OverallQual | OverallCond | YearBuilt | YearRemodAdd | MasVnrArea | BsmtFinSF1 | ... | WoodDeckSF | OpenPorchSF | EnclosedPorch | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SalePrice | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 1460.000000 | 1460.000000 | 1201.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1452.000000 | 1460.000000 | ... | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 |

| mean | 730.500000 | 56.897260 | 70.049958 | 10516.828082 | 6.099315 | 5.575342 | 1971.267808 | 1984.865753 | 103.685262 | 443.639726 | ... | 94.244521 | 46.660274 | 21.954110 | 3.409589 | 15.060959 | 2.758904 | 43.489041 | 6.321918 | 2007.815753 | 180921.195890 |

| std | 421.610009 | 42.300571 | 24.284752 | 9981.264932 | 1.382997 | 1.112799 | 30.202904 | 20.645407 | 181.066207 | 456.098091 | ... | 125.338794 | 66.256028 | 61.119149 | 29.317331 | 55.757415 | 40.177307 | 496.123024 | 2.703626 | 1.328095 | 79442.502883 |

| min | 1.000000 | 20.000000 | 21.000000 | 1300.000000 | 1.000000 | 1.000000 | 1872.000000 | 1950.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 1.000000 | 2006.000000 | 34900.000000 |

| 25% | 365.750000 | 20.000000 | 59.000000 | 7553.500000 | 5.000000 | 5.000000 | 1954.000000 | 1967.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 5.000000 | 2007.000000 | 129975.000000 |

| 50% | 730.500000 | 50.000000 | 69.000000 | 9478.500000 | 6.000000 | 5.000000 | 1973.000000 | 1994.000000 | 0.000000 | 383.500000 | ... | 0.000000 | 25.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 6.000000 | 2008.000000 | 163000.000000 |

| 75% | 1095.250000 | 70.000000 | 80.000000 | 11601.500000 | 7.000000 | 6.000000 | 2000.000000 | 2004.000000 | 166.000000 | 712.250000 | ... | 168.000000 | 68.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 8.000000 | 2009.000000 | 214000.000000 |

| max | 1460.000000 | 190.000000 | 313.000000 | 215245.000000 | 10.000000 | 9.000000 | 2010.000000 | 2010.000000 | 1600.000000 | 5644.000000 | ... | 857.000000 | 547.000000 | 552.000000 | 508.000000 | 480.000000 | 738.000000 | 15500.000000 | 12.000000 | 2010.000000 | 755000.000000 |

8 rows × 38 columns

df_train.shape

(1460, 81)

Before we start, let’s drop Id since it is unnecessary for our analysis.

df_train.drop('Id', axis=1, inplace=True)

df_train.describe()

| MSSubClass | LotFrontage | LotArea | OverallQual | OverallCond | YearBuilt | YearRemodAdd | MasVnrArea | BsmtFinSF1 | BsmtFinSF2 | ... | WoodDeckSF | OpenPorchSF | EnclosedPorch | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SalePrice | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 1460.000000 | 1201.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1452.000000 | 1460.000000 | 1460.000000 | ... | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 | 1460.000000 |

| mean | 56.897260 | 70.049958 | 10516.828082 | 6.099315 | 5.575342 | 1971.267808 | 1984.865753 | 103.685262 | 443.639726 | 46.549315 | ... | 94.244521 | 46.660274 | 21.954110 | 3.409589 | 15.060959 | 2.758904 | 43.489041 | 6.321918 | 2007.815753 | 180921.195890 |

| std | 42.300571 | 24.284752 | 9981.264932 | 1.382997 | 1.112799 | 30.202904 | 20.645407 | 181.066207 | 456.098091 | 161.319273 | ... | 125.338794 | 66.256028 | 61.119149 | 29.317331 | 55.757415 | 40.177307 | 496.123024 | 2.703626 | 1.328095 | 79442.502883 |

| min | 20.000000 | 21.000000 | 1300.000000 | 1.000000 | 1.000000 | 1872.000000 | 1950.000000 | 0.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 1.000000 | 2006.000000 | 34900.000000 |

| 25% | 20.000000 | 59.000000 | 7553.500000 | 5.000000 | 5.000000 | 1954.000000 | 1967.000000 | 0.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 5.000000 | 2007.000000 | 129975.000000 |

| 50% | 50.000000 | 69.000000 | 9478.500000 | 6.000000 | 5.000000 | 1973.000000 | 1994.000000 | 0.000000 | 383.500000 | 0.000000 | ... | 0.000000 | 25.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 6.000000 | 2008.000000 | 163000.000000 |

| 75% | 70.000000 | 80.000000 | 11601.500000 | 7.000000 | 6.000000 | 2000.000000 | 2004.000000 | 166.000000 | 712.250000 | 0.000000 | ... | 168.000000 | 68.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 8.000000 | 2009.000000 | 214000.000000 |

| max | 190.000000 | 313.000000 | 215245.000000 | 10.000000 | 9.000000 | 2010.000000 | 2010.000000 | 1600.000000 | 5644.000000 | 1474.000000 | ... | 857.000000 | 547.000000 | 552.000000 | 508.000000 | 480.000000 | 738.000000 | 15500.000000 | 12.000000 | 2010.000000 | 755000.000000 |

8 rows × 37 columns

Dropping Outliers

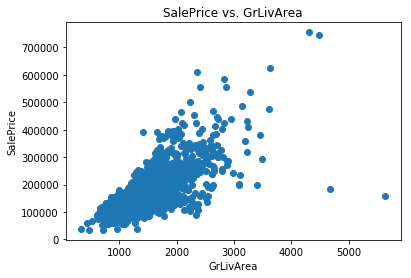

The dataset documentation indicates that there are five outliers that should be removed prior to proceeding with the data (four in the training set). These outliers can be easily seen from the scatter plot of SalePrice vs. GrLivArea. Let’s write a simple function that allows us to easily plot a single scatter plot.

# Function to easily plot a single scatter plot

def scatter_plot_single(df, target, col):

plt.scatter(x=df[col], y=df[target])

plt.xlabel(col)

plt.ylabel(target)

plt.title(target + ' vs. ' + col)

scatter_plot_single(df_train, 'SalePrice', 'GrLivArea')

We can see the four outliers in question. Two of them are very low-priced houses with a high GrLivArea. The other three simply appear to be expensive houses that are still following the trend. The documentation recommends us to get rid of these outliers before processing the data further, so let’s do that.

# Check shape

df_train.shape

(1460, 80)

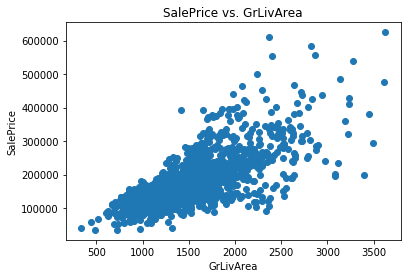

df_train = df_train.drop(df_train[(df_train['GrLivArea']>4000)].index)

# Check shape again

df_train.shape

(1456, 80)

# Plot again for visual check

scatter_plot_single(df_train, 'SalePrice', 'GrLivArea')

# Check shape

df_train.shape

(1456, 80)

Exploring the Data

Univariate Data

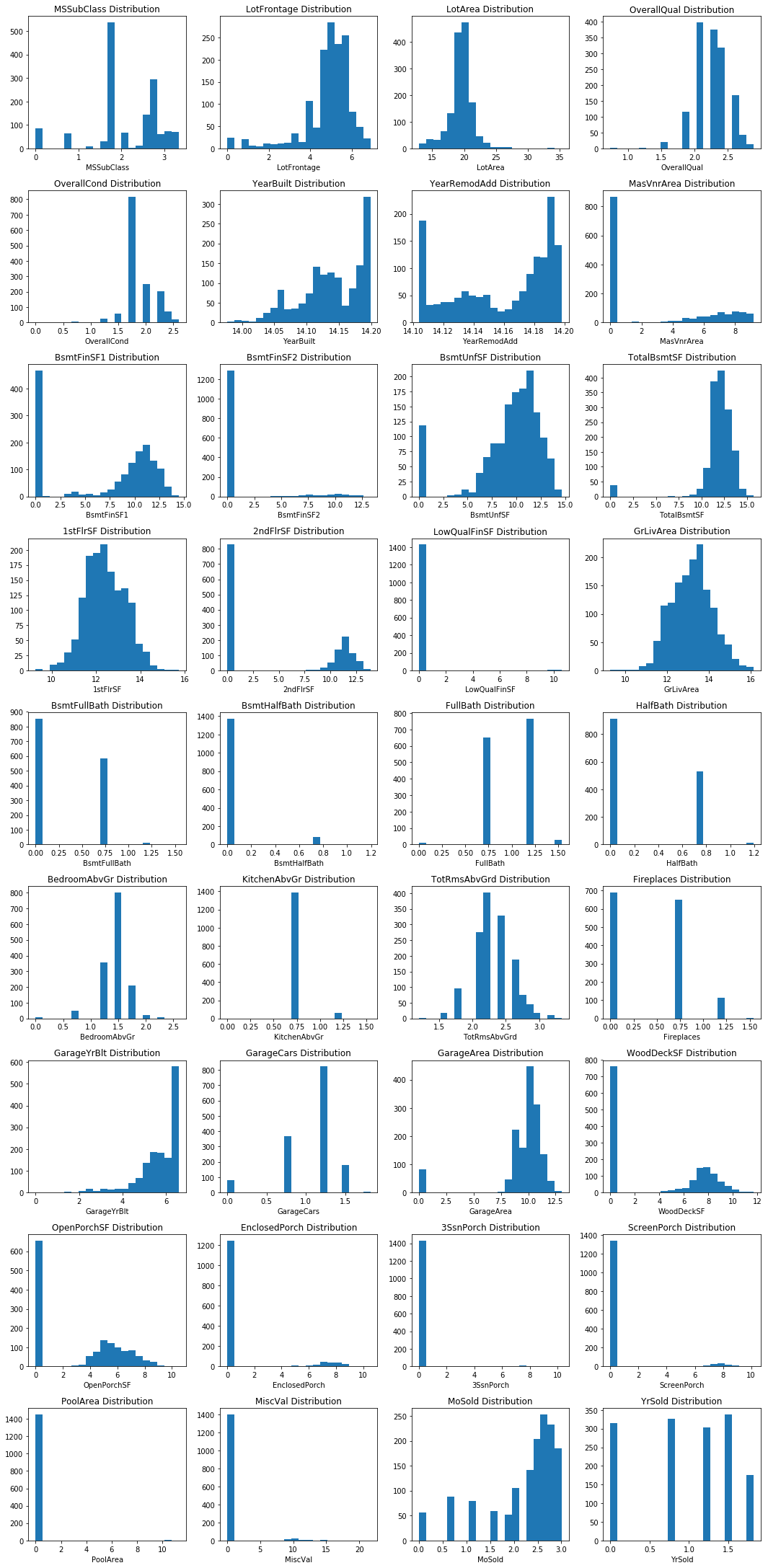

Let’s plot the distributions for each of our continuous features. We can write a function to do this.

cols = ['MSSubClass', 'LotFrontage', 'LotArea', 'OverallQual', 'OverallCond',

'YearBuilt', 'YearRemodAdd', 'MasVnrArea', 'BsmtFinSF1', 'BsmtFinSF2',

'BsmtUnfSF', 'TotalBsmtSF', '1stFlrSF', '2ndFlrSF', 'LowQualFinSF',

'GrLivArea', 'BsmtFullBath', 'BsmtHalfBath', 'FullBath', 'HalfBath',

'BedroomAbvGr', 'KitchenAbvGr', 'TotRmsAbvGrd', 'Fireplaces', 'GarageYrBlt',

'GarageCars', 'GarageArea', 'WoodDeckSF', 'OpenPorchSF', 'EnclosedPorch',

'3SsnPorch', 'ScreenPorch', 'PoolArea', 'MiscVal', 'MoSold', 'YrSold']

# Function to neatly plot multiple histograms

def histogram_multiple(df, cols, figsize_x, figsize_y, nrows, ncols):

i = 1

plt.figure(figsize=(figsize_x, figsize_y))

for col in cols:

plt.subplot(nrows,ncols,i)

plt.hist(df[col], bins=20)

plt.xlabel(col)

plt.title(col + ' Distribution')

i += 1

plt.tight_layout()

plt.show()

histogram_multiple(df_train, cols, 15, 50, 15, 4)

Feature-Target Relationships

Continuous Features

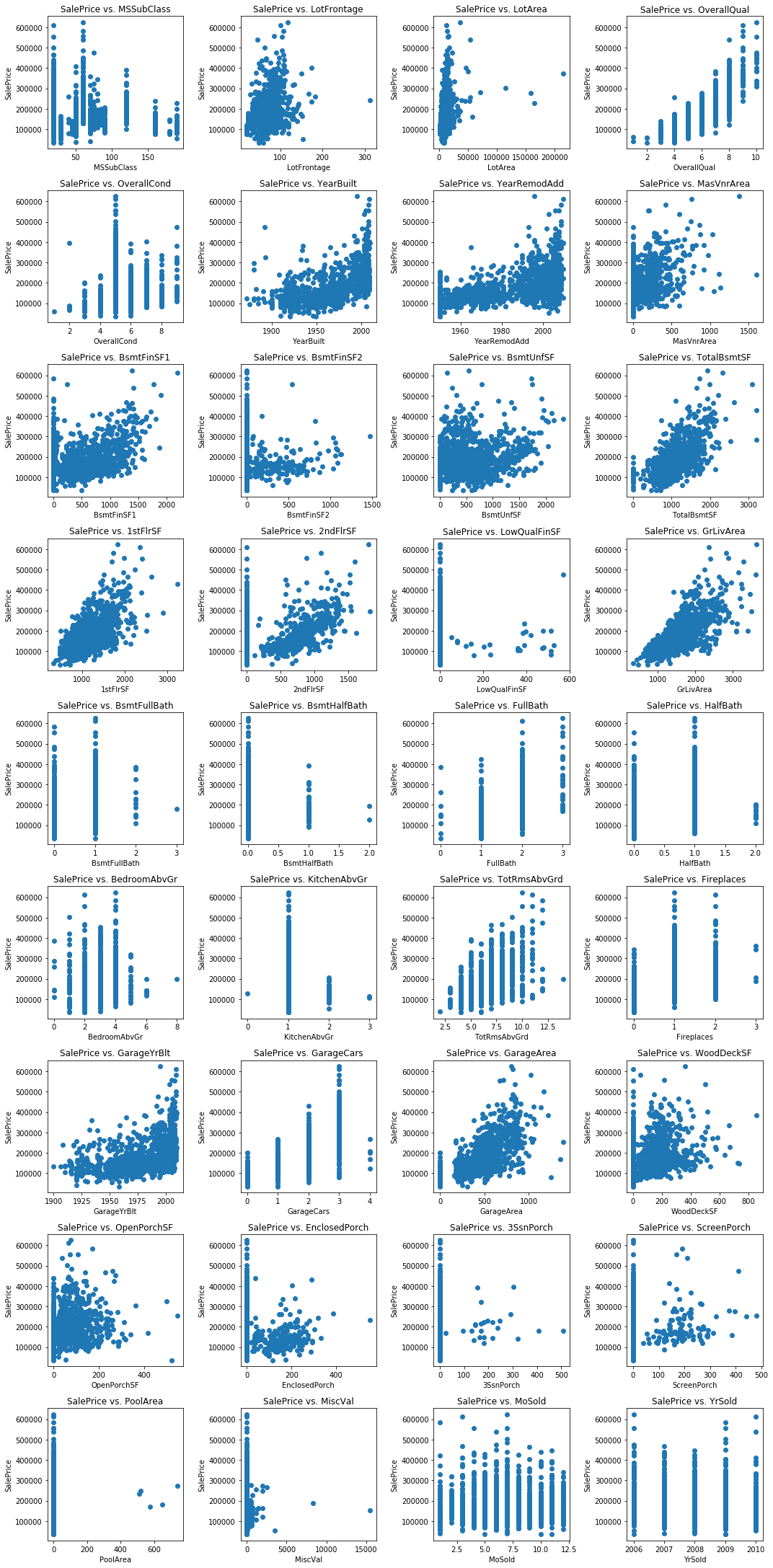

Now let’s visualize the relationship between SalePrice and all of our continuous features. We can write a function to easily create a scatter plot for any given x and y with our desired parameters. First let’s put all the column names for our continuous variables into a list.

# Function to easily plot a single scatter plot

def scatter_plot_single(df, target, col):

plt.scatter(x=df[col], y=df[target])

plt.xlabel(col)

plt.ylabel(target)

plt.title(target + ' vs. ' + col)

# Function to neatly plot multiple scatter plots

def scatter_plot_multiple(df, target, cols, figsize_x, figsize_y, nrows, ncols):

i = 1

plt.figure(figsize=(figsize_x, figsize_y))

for col in cols:

if col != target:

plt.subplot(nrows,ncols,i)

scatter_plot_single(df, target, col)

i += 1

plt.tight_layout()

plt.show()

Now we can use this to neatly visualize scatter plots of SalePrice with many different input features all in one place. For the amount of features we have, we can use nine rows and four columns.

df_train.head()

| MSSubClass | MSZoning | LotFrontage | LotArea | Street | Alley | LotShape | LandContour | Utilities | LotConfig | ... | PoolArea | PoolQC | Fence | MiscFeature | MiscVal | MoSold | YrSold | SaleType | SaleCondition | SalePrice | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 60 | RL | 65.0 | 8450 | Pave | NaN | Reg | Lvl | AllPub | Inside | ... | 0 | NaN | NaN | NaN | 0 | 2 | 2008 | WD | Normal | 208500 |

| 1 | 20 | RL | 80.0 | 9600 | Pave | NaN | Reg | Lvl | AllPub | FR2 | ... | 0 | NaN | NaN | NaN | 0 | 5 | 2007 | WD | Normal | 181500 |

| 2 | 60 | RL | 68.0 | 11250 | Pave | NaN | IR1 | Lvl | AllPub | Inside | ... | 0 | NaN | NaN | NaN | 0 | 9 | 2008 | WD | Normal | 223500 |

| 3 | 70 | RL | 60.0 | 9550 | Pave | NaN | IR1 | Lvl | AllPub | Corner | ... | 0 | NaN | NaN | NaN | 0 | 2 | 2006 | WD | Abnorml | 140000 |

| 4 | 60 | RL | 84.0 | 14260 | Pave | NaN | IR1 | Lvl | AllPub | FR2 | ... | 0 | NaN | NaN | NaN | 0 | 12 | 2008 | WD | Normal | 250000 |

5 rows × 80 columns

continuous_feature_names = df_train.select_dtypes(['float64','int64']).columns

scatter_plot_multiple(df_train, 'SalePrice', continuous_feature_names, 15, 50, 15, 4)

The following features exhibit a strong linear relationship with SalePrice:

- LotFrontage

- TotalBsmtSF

- 1stFlrSF

- GrLivArea

- GarageArea

The following features exhibit a weak linear relationship with SalePrice:

- LotArea

- MasVnrArea

- BsmtFinSF1

- BsmtUnfSF

- WoodDeckSF

- OpenPorchSF

- PoolArea

We will transform the nonlinear features in order to linearize them prior to modeling.

Categorical Features

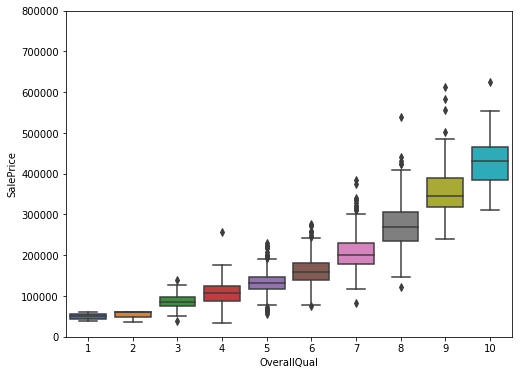

Now let’s visualize some categorical variables to see how they relate to SalePrice. First let’s plot a boxplot of SalePrice vs. OverallQual.

var = 'OverallQual'

data = pd.concat([df_train['SalePrice'], df_train[var]], axis=1)

f, ax = plt.subplots(figsize=(8, 6))

fig = sns.boxplot(x=var, y="SalePrice", data=data)

fig.axis(ymin=0, ymax=800000);

We can clearly see that as the owner-reported overall quality rating increases, the SalePrice increases as well, which makes sense. We would expect higher-priced homes to be of better quality. Now let’s take a look at SalePrice vs. YearBuilt.

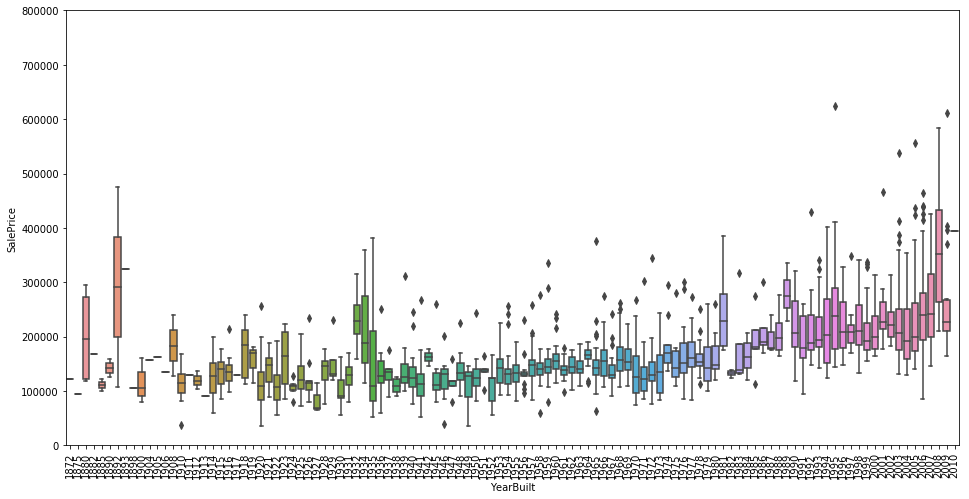

var = 'YearBuilt'

data = pd.concat([df_train['SalePrice'], df_train[var]], axis=1)

f, ax = plt.subplots(figsize=(16, 8))

fig = sns.boxplot(x=var, y="SalePrice", data=data)

fig.axis(ymin=0, ymax=800000);

plt.xticks(rotation=90);

The home selling price does appear to increase slightly over time, aside from some odd outliers at the far left end of the scale (late 1800s).

Our target variable is SalePrice, so our objective will be to predict a home’s selling price based on the given input features. We will place an emphasis on feature engineering to maximize model accuracy.

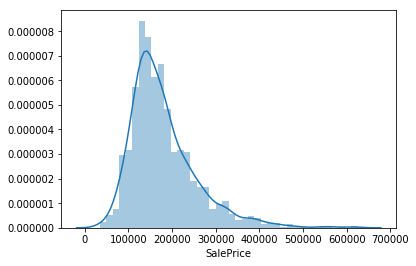

Analysis of SalePrice

Let’s take a closer look at our target variable.

df_train['SalePrice'].describe()

count 1456.000000

mean 180151.233516

std 76696.592530

min 34900.000000

25% 129900.000000

50% 163000.000000

75% 214000.000000

max 625000.000000

Name: SalePrice, dtype: float64

df_train[df_train.SalePrice == df_train.SalePrice.max()]

| MSSubClass | MSZoning | LotFrontage | LotArea | Street | Alley | LotShape | LandContour | Utilities | LotConfig | ... | PoolArea | PoolQC | Fence | MiscFeature | MiscVal | MoSold | YrSold | SaleType | SaleCondition | SalePrice | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1169 | 60 | RL | 118.0 | 35760 | Pave | NaN | IR1 | Lvl | AllPub | CulDSac | ... | 0 | NaN | NaN | NaN | 0 | 7 | 2006 | WD | Normal | 625000 |

1 rows × 80 columns

sns.distplot(df_train['SalePrice']);

SalePrice deviates from a normal distribution and appears to be right-skewed. Linear models perform better with normally distributed data, so we should transform this variable. We can use the numpy.log1p() function to transform the data so that it is accurate for a wide range of floating point values. This is equivalent to ln(1+p), which allows us to include 0 values.

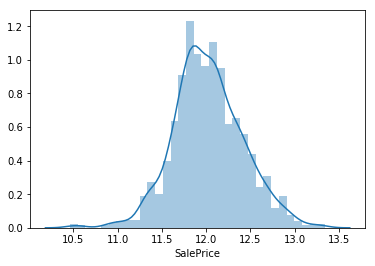

df_train['SalePrice'] = np.log1p(df_train['SalePrice'])

# Check the distribution again

sns.distplot(df_train['SalePrice']);

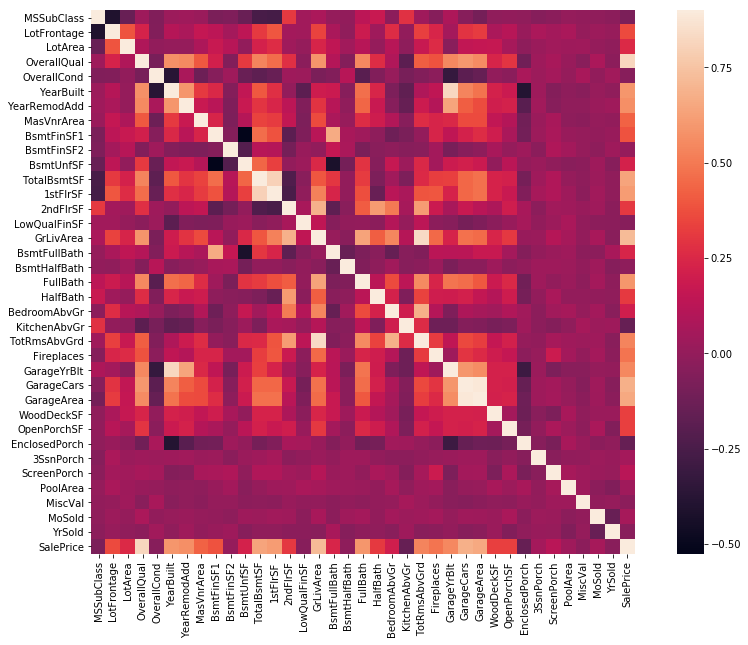

Correlation Heatmap

# Correlation map

corr = df_train.corr()

plt.subplots(figsize=(15,10))

sns.heatmap(corr, vmax=0.8, square=True)

<matplotlib.axes._subplots.AxesSubplot at 0x11c64a1d0>

Most of the variables appear to be moderately correlated.

Feature Engineering

Handle Missing Values

We will impute the missing values for each feature. First, let’s see how many missing values there are.

# Missing data

total = df_train.isnull().sum().sort_values(ascending=False)

percent = (df_train.isnull().sum()/df_train.isnull().count()).sort_values(ascending=False)

missing_data = pd.concat([total, percent], axis=1, keys=['Total', 'Percent'])

missing_data.head(20)

| Total | Percent | |

|---|---|---|

| PoolQC | 1451 | 0.996566 |

| MiscFeature | 1402 | 0.962912 |

| Alley | 1365 | 0.937500 |

| Fence | 1176 | 0.807692 |

| FireplaceQu | 690 | 0.473901 |

| LotFrontage | 259 | 0.177885 |

| GarageType | 81 | 0.055632 |

| GarageCond | 81 | 0.055632 |

| GarageFinish | 81 | 0.055632 |

| GarageQual | 81 | 0.055632 |

| GarageYrBlt | 81 | 0.055632 |

| BsmtFinType2 | 38 | 0.026099 |

| BsmtExposure | 38 | 0.026099 |

| BsmtQual | 37 | 0.025412 |

| BsmtCond | 37 | 0.025412 |

| BsmtFinType1 | 37 | 0.025412 |

| MasVnrArea | 8 | 0.005495 |

| MasVnrType | 8 | 0.005495 |

| Electrical | 1 | 0.000687 |

| RoofMatl | 0 | 0.000000 |

PoolQC, MiscFeature, Alley, Fence, FireplaceQu

Since these features have a significant percentage of null values (>40%), we can safely just drop them entirely.

df_train = df_train.drop(['PoolQC', 'MiscFeature', 'Alley','Fence', 'FireplaceQu'], axis=1)

LotFrontage

We can assume that homes in the same neighborhood will have similar values for the linear feet of street connected to their property. Thus, we can use groupby to group according to neighborhood and fill in the missing values with the median LotFrontage.

df_train['LotFrontage'] = df_train.groupby('Neighborhood')['LotFrontage'].transform(lambda x: x.fillna(x.median()))

df_train['LotFrontage'].describe()

count 1456.000000

mean 69.895948

std 21.331035

min 21.000000

25% 60.000000

50% 70.000000

75% 80.000000

max 313.000000

Name: LotFrontage, dtype: float64

GarageType, GarageCond, GarageFinish, GarageQual, GarageYrBlt

For each of the categorical garage features, we can fill in the missing values with ‘None’, since it indicates no garage.

for col in ['GarageType', 'GarageFinish', 'GarageQual', 'GarageCond', 'GarageYrBlt']:

df_train[col] = df_train[col].fillna('None')

BsmtQual, BsmtCond, BsmtFinType1

For these three basement features, we can fill in the missing values with ‘None’.

for col in ['BsmtQual', 'BsmtCond', 'BsmtFinType1']:

df_train[col] = df_train[col].fillna('None')

BsmtFinType2, BsmtExposure

For these two basement features, we can fill in the missing values with ‘None’.

for col in ['BsmtFinType2', 'BsmtExposure']:

df_train[col] = df_train[col].fillna('None')

MasVnrArea

A value of NaN means no masonry veneer for the home, so we can fill in missing values with 0.

df_train['MasVnrArea'] = df_train['MasVnrArea'].fillna(0)

MsVnrType

A value of NaN means no masonry veneer for the home, so we can fill in missing values with ‘None’.

df_train['MasVnrType'] = df_train['MasVnrType'].fillna('None')

Utilities

All of the values are ‘AllPub’ except for three of them. Therefore, this feature will not be useful for modeling, and we can safely drop it.

df_train = df_train.drop(['Utilities'], axis=1)

Functional

According to the data description, a value of NaN means typical. Thus, we can replace missing values with ‘Typ’.

df_train['Functional'] = df_train['Functional'].fillna('Typ')

Electrical

There is only one NaN value, so we can replace it with the most frequently occurring value, ‘SBrkr’.

df_train['Electrical'] = df_train['Electrical'].fillna(df_train['Electrical'].mode()[0])

# Check missing data

total = df_train.isnull().sum().sort_values(ascending=False)

percent = (df_train.isnull().sum()/df_train.isnull().count()).sort_values(ascending=False)

missing_data = pd.concat([total, percent], axis=1, keys=['Total', 'Percent'])

missing_data.head(19)

| Total | Percent | |

|---|---|---|

| SalePrice | 0 | 0.0 |

| RoofStyle | 0 | 0.0 |

| Exterior1st | 0 | 0.0 |

| Exterior2nd | 0 | 0.0 |

| MasVnrType | 0 | 0.0 |

| MasVnrArea | 0 | 0.0 |

| ExterQual | 0 | 0.0 |

| ExterCond | 0 | 0.0 |

| Foundation | 0 | 0.0 |

| BsmtQual | 0 | 0.0 |

| BsmtCond | 0 | 0.0 |

| BsmtExposure | 0 | 0.0 |

| BsmtFinType1 | 0 | 0.0 |

| BsmtFinSF1 | 0 | 0.0 |

| BsmtFinType2 | 0 | 0.0 |

| BsmtFinSF2 | 0 | 0.0 |

| BsmtUnfSF | 0 | 0.0 |

| RoofMatl | 0 | 0.0 |

| YearRemodAdd | 0 | 0.0 |

df_train.describe()

| MSSubClass | LotFrontage | LotArea | OverallQual | OverallCond | YearBuilt | YearRemodAdd | MasVnrArea | BsmtFinSF1 | BsmtFinSF2 | ... | WoodDeckSF | OpenPorchSF | EnclosedPorch | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SalePrice | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.00000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | ... | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 |

| mean | 56.888736 | 69.895948 | 10448.784341 | 6.088599 | 5.576236 | 1971.18544 | 1984.819368 | 101.526786 | 436.991071 | 46.677198 | ... | 93.833791 | 46.221154 | 22.014423 | 3.418956 | 15.102335 | 2.055632 | 43.608516 | 6.326236 | 2007.817308 | 12.021950 |

| std | 42.358363 | 21.331035 | 9860.763449 | 1.369669 | 1.113966 | 30.20159 | 20.652143 | 177.011773 | 430.255052 | 161.522376 | ... | 125.192349 | 65.352424 | 61.192248 | 29.357056 | 55.828405 | 35.383772 | 496.799265 | 2.698356 | 1.329394 | 0.396077 |

| min | 20.000000 | 21.000000 | 1300.000000 | 1.000000 | 1.000000 | 1872.00000 | 1950.000000 | 0.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 1.000000 | 2006.000000 | 10.460271 |

| 25% | 20.000000 | 60.000000 | 7538.750000 | 5.000000 | 5.000000 | 1954.00000 | 1966.750000 | 0.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 5.000000 | 2007.000000 | 11.774528 |

| 50% | 50.000000 | 70.000000 | 9468.500000 | 6.000000 | 5.000000 | 1972.00000 | 1993.500000 | 0.000000 | 381.000000 | 0.000000 | ... | 0.000000 | 24.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 6.000000 | 2008.000000 | 12.001512 |

| 75% | 70.000000 | 80.000000 | 11588.000000 | 7.000000 | 6.000000 | 2000.00000 | 2004.000000 | 163.250000 | 706.500000 | 0.000000 | ... | 168.000000 | 68.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 8.000000 | 2009.000000 | 12.273736 |

| max | 190.000000 | 313.000000 | 215245.000000 | 10.000000 | 9.000000 | 2010.00000 | 2010.000000 | 1600.000000 | 2188.000000 | 1474.000000 | ... | 857.000000 | 547.000000 | 552.000000 | 508.000000 | 480.000000 | 738.000000 | 15500.000000 | 12.000000 | 2010.000000 | 13.345509 |

8 rows × 36 columns

Label Encoding Categorical Features

Since there are categorical features that depend on ordering (such as YrSold), we can encode all the categorical features using label encoding, which accounts for ordering.

# Convert some numerical features to categorical

for col in ['MSSubClass', 'OverallCond', 'YrSold', 'MoSold']:

df_train[col] = df_train[col].apply(str)

print(df_train.dtypes)

MSSubClass int64

MSZoning int64

LotFrontage float64

LotArea int64

Street int64

LotShape object

LandContour object

LotConfig object

LandSlope object

Neighborhood object

Condition1 object

Condition2 object

BldgType object

HouseStyle object

OverallQual int64

OverallCond object

YearBuilt int64

YearRemodAdd int64

RoofStyle object

RoofMatl object

Exterior1st object

Exterior2nd object

MasVnrType object

MasVnrArea float64

ExterQual object

ExterCond object

Foundation object

BsmtQual object

BsmtCond object

BsmtExposure object

BsmtFinType1 object

BsmtFinSF1 int64

BsmtFinType2 object

BsmtFinSF2 int64

BsmtUnfSF int64

TotalBsmtSF int64

Heating object

HeatingQC object

CentralAir object

Electrical object

1stFlrSF int64

2ndFlrSF int64

LowQualFinSF int64

GrLivArea int64

BsmtFullBath int64

BsmtHalfBath int64

FullBath int64

HalfBath int64

BedroomAbvGr int64

KitchenAbvGr int64

KitchenQual object

TotRmsAbvGrd int64

Functional object

Fireplaces int64

GarageType object

GarageYrBlt object

GarageFinish object

GarageCars int64

GarageArea int64

GarageQual object

GarageCond object

PavedDrive object

WoodDeckSF int64

OpenPorchSF int64

EnclosedPorch int64

3SsnPorch int64

ScreenPorch int64

PoolArea int64

MiscVal int64

MoSold object

YrSold object

SaleType object

SaleCondition object

SalePrice float64

dtype: object

cols = ['MSSubClass', 'MSZoning', 'LotFrontage', 'Street', 'LotShape', 'LandContour', 'LotConfig',

'LandSlope', 'Neighborhood', 'Condition1', 'Condition2', 'BldgType', 'HouseStyle', 'OverallCond', 'RoofStyle',

'RoofMatl', 'Exterior1st', 'Exterior2nd', 'MasVnrType', 'MasVnrArea', 'ExterQual', 'ExterCond', 'Foundation',

'BsmtQual', 'BsmtCond', 'BsmtExposure', 'BsmtFinType1', 'BsmtFinType2', 'Heating', 'HeatingQC', 'CentralAir',

'Electrical', 'KitchenQual', 'Functional', 'GarageType', 'GarageYrBlt', 'GarageFinish', 'GarageQual',

'GarageCond', 'PavedDrive', 'MoSold', 'YrSold', 'SaleType', 'SaleCondition']

# Apply LabelEncoder to categorical features

for col in cols:

le = LabelEncoder()

le.fit(list(df_train[col].values))

df_train[col] = le.transform(list(df_train[col].values))

Add TotalSF Feature

Let’s add a feature for the total square footage.

# Add feature for total square footage

df_train['TotalSF'] = df_train['TotalBsmtSF'] + df_train['1stFlrSF'] + df_train['2ndFlrSF']

Transform Skewed Features

In order to transform the features which deviate from a normal distribution, we must use a transformation. A log transformation is a possibility, but I decided to settle on the box-cox transformation, which is more flexible.

# Create a DataFrame of numerical features

numeric_features = df_train.dtypes[df_train.dtypes != 'object'].index

# Check the skew of numerical features

skewed_features = df_train[numeric_features].apply(lambda x: skew(x)).sort_values(ascending=False)

skewness = pd.DataFrame({'Skew': skewed_features})

skewness.head(10)

| Skew | |

|---|---|

| MiscVal | 24.418175 |

| PoolArea | 17.504556 |

| Condition2 | 13.666839 |

| LotArea | 12.574590 |

| 3SsnPorch | 10.279262 |

| Heating | 9.831083 |

| LowQualFinSF | 8.989291 |

| RoofMatl | 8.293646 |

| LandSlope | 4.801326 |

| KitchenAbvGr | 4.476748 |

# Include features that have a skewness greater than 0.75

skewness = skewness[abs(skewness) > 0.75]

print('Total skewed features: {}'.format(skewness.shape[0]))

skewed_features = skewness.index

alpha = 0.15

for feature in skewed_features:

df_train[feature] = boxcox1p(df_train[feature], alpha)

Total skewed features: 75

# Convert categorical variable into dummy

df_train = pd.get_dummies(df_train)

df_train.head()

| MSSubClass | MSZoning | LotFrontage | LotArea | Street | LotShape | LandContour | LotConfig | LandSlope | Neighborhood | ... | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SaleType | SaleCondition | SalePrice | TotalSF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2.750250 | 1.540963 | 4.882973 | 19.212182 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 0.0 | 2.055642 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 1.820334 | 1.194318 | 2.602594 | 1.820334 | 3.156009 | 14.976591 |

| 1 | 1.820334 | 1.540963 | 5.527074 | 19.712205 | 0.730463 | 1.540963 | 1.540963 | 1.194318 | 0.0 | 4.137711 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 2.440268 | 0.730463 | 2.602594 | 1.820334 | 3.140516 | 14.923100 |

| 2 | 2.750250 | 1.540963 | 5.053371 | 20.347241 | 0.730463 | 0.000000 | 1.540963 | 1.820334 | 0.0 | 2.055642 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 3.011340 | 1.194318 | 2.602594 | 1.820334 | 3.163719 | 15.149678 |

| 3 | 2.885846 | 1.540963 | 4.545286 | 19.691553 | 0.730463 | 0.000000 | 1.540963 | 0.000000 | 0.0 | 2.259674 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 1.820334 | 0.000000 | 2.602594 | 0.000000 | 3.111134 | 14.857121 |

| 4 | 2.750250 | 1.540963 | 5.653921 | 21.325160 | 0.730463 | 0.000000 | 1.540963 | 1.194318 | 0.0 | 3.438110 | ... | 0.0 | 0.0 | 0.0 | 0.0 | 1.540963 | 1.194318 | 2.602594 | 1.820334 | 3.176081 | 15.852312 |

5 rows × 75 columns

df_train.describe()

| MSSubClass | MSZoning | LotFrontage | LotArea | Street | LotShape | LandContour | LotConfig | LandSlope | Neighborhood | ... | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SaleType | SaleCondition | SalePrice | TotalSF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | ... | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 |

| mean | 2.120462 | 1.532216 | 4.838973 | 19.545432 | 0.727453 | 1.006929 | 1.439999 | 1.403936 | 0.043274 | 2.993064 | ... | 0.131088 | 0.624309 | 0.036790 | 0.403946 | 2.211254 | 0.988608 | 2.478930 | 1.703198 | 3.130140 | 14.834646 |

| std | 0.804227 | 0.242085 | 1.198320 | 2.025558 | 0.046811 | 0.720319 | 0.338967 | 0.712903 | 0.186299 | 0.799155 | ... | 1.023859 | 2.137374 | 0.627302 | 2.153524 | 0.740955 | 0.623489 | 0.465932 | 0.475669 | 0.044712 | 0.980603 |

| min | 0.000000 | 0.000000 | 0.000000 | 12.878993 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.944763 | 9.279836 |

| 25% | 1.820334 | 1.540963 | 4.545286 | 18.773051 | 0.730463 | 0.000000 | 1.540963 | 1.194318 | 0.000000 | 2.440268 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.055642 | 0.730463 | 2.602594 | 1.820334 | 3.102566 | 14.195323 |

| 50% | 2.055642 | 1.540963 | 5.133567 | 19.657692 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 0.000000 | 3.128239 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.440268 | 1.194318 | 2.602594 | 1.820334 | 3.128410 | 14.855815 |

| 75% | 2.750250 | 1.540963 | 5.527074 | 20.467446 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 0.000000 | 3.618223 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.750250 | 1.540963 | 2.602594 | 1.820334 | 3.158902 | 15.488874 |

| max | 3.340760 | 1.820334 | 6.899104 | 35.391371 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 1.194318 | 4.137711 | ... | 10.312501 | 10.169007 | 11.289160 | 21.677435 | 3.011340 | 1.820334 | 2.602594 | 2.055642 | 3.274014 | 18.172113 |

8 rows × 75 columns

Modeling

For our modeling, we will do three iterations:

- Full feature set

- Reduced feature set

- PCA

In each iteration, we will create five models:

- Linear Regression

- KNN Regression

- Random Forest Regresion

- Ridge Regression

- Lasso Regression

We will generate an accuracy score for each of the models and determine which model most accurately predicts our target variable, SalePrice. For iterations 1 and 2, we will use GridSearchCV to determine the best set of parameters for our model, and for iteration 3, we will use pipe to chain together PCA with our regression model.

X = df_train.drop(['SalePrice'], axis=1)

y = df_train.loc[:, ['SalePrice']]

X.head()

| MSSubClass | MSZoning | LotFrontage | LotArea | Street | LotShape | LandContour | LotConfig | LandSlope | Neighborhood | ... | EnclosedPorch | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SaleType | SaleCondition | TotalSF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2.750250 | 1.540963 | 4.882973 | 19.212182 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 0.0 | 2.055642 | ... | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 1.820334 | 1.194318 | 2.602594 | 1.820334 | 14.976591 |

| 1 | 1.820334 | 1.540963 | 5.527074 | 19.712205 | 0.730463 | 1.540963 | 1.540963 | 1.194318 | 0.0 | 4.137711 | ... | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 2.440268 | 0.730463 | 2.602594 | 1.820334 | 14.923100 |

| 2 | 2.750250 | 1.540963 | 5.053371 | 20.347241 | 0.730463 | 0.000000 | 1.540963 | 1.820334 | 0.0 | 2.055642 | ... | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 3.011340 | 1.194318 | 2.602594 | 1.820334 | 15.149678 |

| 3 | 2.885846 | 1.540963 | 4.545286 | 19.691553 | 0.730463 | 0.000000 | 1.540963 | 0.000000 | 0.0 | 2.259674 | ... | 8.797736 | 0.0 | 0.0 | 0.0 | 0.0 | 1.820334 | 0.000000 | 2.602594 | 0.000000 | 14.857121 |

| 4 | 2.750250 | 1.540963 | 5.653921 | 21.325160 | 0.730463 | 0.000000 | 1.540963 | 1.194318 | 0.0 | 3.438110 | ... | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 1.540963 | 1.194318 | 2.602594 | 1.820334 | 15.852312 |

5 rows × 74 columns

X.describe()

| MSSubClass | MSZoning | LotFrontage | LotArea | Street | LotShape | LandContour | LotConfig | LandSlope | Neighborhood | ... | EnclosedPorch | 3SsnPorch | ScreenPorch | PoolArea | MiscVal | MoSold | YrSold | SaleType | SaleCondition | TotalSF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | ... | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 | 1456.000000 |

| mean | 2.120462 | 1.532216 | 4.838973 | 19.545432 | 0.727453 | 1.006929 | 1.439999 | 1.403936 | 0.043274 | 2.993064 | ... | 1.041125 | 0.131088 | 0.624309 | 0.036790 | 0.403946 | 2.211254 | 0.988608 | 2.478930 | 1.703198 | 14.834646 |

| std | 0.804227 | 0.242085 | 1.198320 | 2.025558 | 0.046811 | 0.720319 | 0.338967 | 0.712903 | 0.186299 | 0.799155 | ... | 2.589720 | 1.023859 | 2.137374 | 0.627302 | 2.153524 | 0.740955 | 0.623489 | 0.465932 | 0.475669 | 0.980603 |

| min | 0.000000 | 0.000000 | 0.000000 | 12.878993 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 9.279836 |

| 25% | 1.820334 | 1.540963 | 4.545286 | 18.773051 | 0.730463 | 0.000000 | 1.540963 | 1.194318 | 0.000000 | 2.440268 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.055642 | 0.730463 | 2.602594 | 1.820334 | 14.195323 |

| 50% | 2.055642 | 1.540963 | 5.133567 | 19.657692 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 0.000000 | 3.128239 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.440268 | 1.194318 | 2.602594 | 1.820334 | 14.855815 |

| 75% | 2.750250 | 1.540963 | 5.527074 | 20.467446 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 0.000000 | 3.618223 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 2.750250 | 1.540963 | 2.602594 | 1.820334 | 15.488874 |

| max | 3.340760 | 1.820334 | 6.899104 | 35.391371 | 0.730463 | 1.540963 | 1.540963 | 1.820334 | 1.194318 | 4.137711 | ... | 10.524981 | 10.312501 | 10.169007 | 11.289160 | 21.677435 | 3.011340 | 1.820334 | 2.602594 | 2.055642 | 18.172113 |

8 rows × 74 columns

y.head()

| SalePrice | |

|---|---|

| 0 | 3.156009 |

| 1 | 3.140516 |

| 2 | 3.163719 |

| 3 | 3.111134 |

| 4 | 3.176081 |

Iteration 1 - All Original Features

In this iteration, we will run our models with the full feature set.

# Split the data into train and test sets

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2)

Linear Regression

# Instantiate model and create parameter grid

lr = linear_model.LinearRegression()

grid_params = {'fit_intercept': [True, False],

'normalize': [True, False],

'copy_X' : [True, False]}

# Instantiate new grid

grid = GridSearchCV(lr, grid_params, n_jobs=-1, cv=5)

# Linear Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 11.0 s

Best Accuracy Score:

0.9038859588435272

Best Parameters:

{'copy_X': True, 'fit_intercept': False, 'normalize': True}

# Instantiate and fit model with best parameters

lr = LinearRegression(fit_intercept=False, normalize=True, copy_X=True)

lr.fit(X_train, y_train)

y_pred = lr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(lr, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(lr.score(X_test, y_test)))

print('Cross Validation Scores:\n', scores)

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

90.03%

Cross Validation Scores:

[0.88870071 0.90088601 0.91468823 0.92236951 0.89273748]

Average Cross Validation Score:

90.39%

Root Mean Squared Error:

0.30628900378557106

KNN Regression

# Instantiate model and create parameter grid

knn = neighbors.KNeighborsRegressor()

grid_params = {'n_neighbors': list(range(1, 10)),

'weights': ['uniform', 'distance'],

'algorithm' : ['auto', 'ball_tree', 'kd_tree', 'brute']}

# Instantiate new grid

grid = GridSearchCV(knn, grid_params, n_jobs=-1, cv=5)

# KNN Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 12.2 s

Best Accuracy Score:

0.6595538969910677

Best Parameters:

{'algorithm': 'brute', 'n_neighbors': 6, 'weights': 'distance'}

# Instantiate and fit model with best parameters

knn = neighbors.KNeighborsRegressor(n_neighbors=5, weights='distance', algorithm='auto')

knn.fit(X_train, y_train)

y_pred = knn.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(knn, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(knn.score(X_test, y_test)))

print('Cross Validation Scores:\n', scores)

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

62.46%

Cross Validation Scores:

[0.64736072 0.64168616 0.65754486 0.67426629 0.65346698]

Average Cross Validation Score:

65.49%

Root Mean Squared Error:

0.612165517811808

Random Forest Regression

# Instantiate model and create parameter grid

rfr = RandomForestRegressor()

grid_params = {'n_estimators': list(range(1, 10)),

'criterion': ['mse', 'mae'],

'max_depth': list(range(1, 10))}

# Instantiate new grid

grid = GridSearchCV(rfr, grid_params, n_jobs=-1, cv=5)

# KNN Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 1.85e+02 s

Best Accuracy Score:

0.8628202929561456

Best Parameters:

{'criterion': 'mse', 'max_depth': 9, 'n_estimators': 8}

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/model_selection/_search.py:714: DataConversionWarning: A column-vector y was passed when a 1d array was expected. Please change the shape of y to (n_samples,), for example using ravel().

self.best_estimator_.fit(X, y, **fit_params)

# Instantiate and fit model with best parameters

rfr = RandomForestRegressor(n_estimators=9, criterion='mse', max_depth=9)

rfr.fit(X_train, y_train.values.ravel())

y_pred = rfr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(rfr, X_train, y_train.values.ravel(), cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(rfr.score(X_test, y_test.values.ravel())))

print('Cross Validation Scores:\n{}'.format(scores))

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

85.10%

Cross Validation Scores:

[0.84404563 0.85909811 0.87318738 0.88366671 0.84070214]

Average Cross Validation Score:

86.01%

Root Mean Squared Error:

0.37838092392711603

Ridge Regression

# Instantiate model and create parameter grid

rr = Ridge()

grid_params = {'alpha': [0.0001, 0.001, 0.01, 0.1, 1, 5, 10, 25, 50, 100],

'fit_intercept': [True, False],

'solver': ['cholesky', 'lsqr', 'sparse_cg']}

# 'solver': ['svd', 'cholesky', 'lsqr', 'sparse_cg', 'sag', 'saga']}

# Instantiate new grid

grid = GridSearchCV(rr, grid_params, n_jobs=-1, cv=5)

# Ridge Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 3.84 s

Best Accuracy Score:

0.9047617389686792

Best Parameters:

{'alpha': 1, 'fit_intercept': False, 'solver': 'cholesky'}

# Instantiate and fit model with best parameters

rr = Ridge(alpha=1, fit_intercept=False, solver='cholesky')

rr.fit(X_train, y_train)

y_pred = rr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(rr, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(rr.score(X_test, y_test)))

print('Cross Validation Scores:\n{}'.format(scores))

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

90.06%

Cross Validation Scores:

[0.8875597 0.90103579 0.91604279 0.92492845 0.89419661]

Average Cross Validation Score:

90.48%

Root Mean Squared Error:

0.3062108626753103

Lasso Regression

# Instantiate model and create parameter grid

lasso = Lasso()

grid_params = {'alpha': [0.0001, 0.001, 0.01, 0.1, 1, 5, 10, 25, 50, 100],

'fit_intercept': [True, False],

'max_iter': list(range(10))}

# 'solver': ['svd', 'cholesky', 'lsqr', 'sparse_cg', 'sag', 'saga']}

# Instantiate new grid

grid = GridSearchCV(lasso, grid_params, n_jobs=-1, cv=5)

# Ridge Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 11.0 s

Best Accuracy Score:

0.8898671924495875

Best Parameters:

{'alpha': 0.0001, 'fit_intercept': True, 'max_iter': 9}

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/model_selection/_search.py:813: DeprecationWarning: The default of the `iid` parameter will change from True to False in version 0.22 and will be removed in 0.24. This will change numeric results when test-set sizes are unequal.

DeprecationWarning)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.13095565812133875, tolerance: 0.0002336781715295783

positive)

# Instantiate and fit model with best parameters

lasso = Lasso(alpha=0.0001, fit_intercept=True, max_iter=9)

lasso.fit(X_train, y_train)

y_pred = rr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(lasso, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(rr.score(X_test, y_test)))

print('Cross Validation Scores:\n{}'.format(scores))

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

90.06%

Cross Validation Scores:

[0.87973372 0.87451241 0.90024551 0.91381628 0.88098994]

Average Cross Validation Score:

88.99%

Root Mean Squared Error:

0.3062108626753103

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.13095565812133875, tolerance: 0.0002336781715295783

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10424985154274628, tolerance: 0.00019337793314266012

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10145213039752624, tolerance: 0.0001859706045300572

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10570657513985911, tolerance: 0.0001856118913612857

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10555805840971894, tolerance: 0.00018213605478717467

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.1016345070657701, tolerance: 0.00018743708089921418

positive)

Our best model in this iteration was Ridge Regression with an accuracy score of 90.06% and an RMSE of 0.30621.

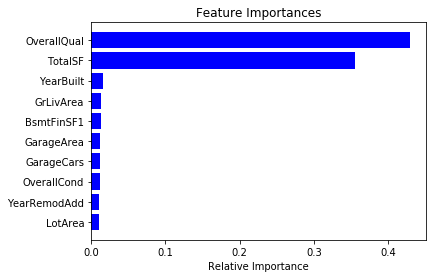

Iteration 2 - Feature Importances

In this iteration, we will use the feature importances from our Random Forest Regressor and extract the 20 most important features. Then, we will re-run all the models above on the reduced feature set.

features = X.columns

importances = rfr.feature_importances_

indices = np.argsort(importances)[-10:] # top 10 features

plt.title('Feature Importances')

plt.barh(range(len(indices)), importances[indices], color='b', align='center')

plt.yticks(range(len(indices)), [features[i] for i in indices])

plt.xlabel('Relative Importance')

plt.show()

feature_importances = pd.DataFrame(rfr.feature_importances_, index = X.columns,

columns=['importance']).sort_values('importance',ascending=False)

feature_importances.head(20)

| importance | |

|---|---|

| OverallQual | 0.429685 |

| TotalSF | 0.355861 |

| YearBuilt | 0.015554 |

| GrLivArea | 0.013061 |

| BsmtFinSF1 | 0.012794 |

| GarageArea | 0.011899 |

| GarageCars | 0.011873 |

| OverallCond | 0.011585 |

| YearRemodAdd | 0.011061 |

| LotArea | 0.010480 |

| BsmtUnfSF | 0.009619 |

| CentralAir | 0.009562 |

| GarageYrBlt | 0.006496 |

| 1stFlrSF | 0.006414 |

| GarageType | 0.006077 |

| Fireplaces | 0.005345 |

| LotFrontage | 0.004462 |

| 2ndFlrSF | 0.003897 |

| SaleCondition | 0.003872 |

| Neighborhood | 0.003725 |

X_reduced = X[['OverallQual', 'TotalSF', 'YearRemodAdd', 'GarageArea', 'CentralAir', 'GrLivArea',

'BsmtFinSF1', 'OverallCond', 'LotArea', 'GarageCond', 'YearBuilt', 'MSZoning',

'1stFlrSF', 'BsmtUnfSF', 'GarageType', 'GarageCars', 'BsmtFinType1', 'LotFrontage',

'BsmtQual', 'GarageYrBlt']]

X_reduced.head()

| OverallQual | TotalSF | YearRemodAdd | GarageArea | CentralAir | GrLivArea | BsmtFinSF1 | OverallCond | LotArea | GarageCond | YearBuilt | MSZoning | 1stFlrSF | BsmtUnfSF | GarageType | GarageCars | BsmtFinType1 | LotFrontage | BsmtQual | GarageYrBlt | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2.440268 | 14.976591 | 14.187527 | 10.506271 | 0.730463 | 13.698888 | 11.170327 | 1.820334 | 19.212182 | 2.055642 | 14.187527 | 1.540963 | 11.692623 | 7.483296 | 0.730463 | 1.194318 | 1.194318 | 4.882973 | 1.194318 | 6.426513 |

| 1 | 2.259674 | 14.923100 | 14.145138 | 10.062098 | 0.730463 | 12.792276 | 12.062832 | 2.440268 | 19.712205 | 2.055642 | 14.145138 | 1.540963 | 12.792276 | 8.897844 | 0.730463 | 1.194318 | 0.000000 | 5.527074 | 1.194318 | 5.744420 |

| 2 | 2.440268 | 15.149678 | 14.185966 | 10.775536 | 0.730463 | 13.832085 | 10.200343 | 1.820334 | 20.347241 | 2.055642 | 14.184404 | 1.540963 | 11.892039 | 9.917060 | 0.730463 | 1.194318 | 1.194318 | 5.053371 | 1.194318 | 6.382451 |

| 3 | 2.440268 | 14.857121 | 14.135652 | 10.918253 | 0.730463 | 13.711364 | 8.274266 | 1.820334 | 19.691553 | 2.055642 | 14.047529 | 1.540963 | 12.013683 | 10.468500 | 2.055642 | 1.540963 | 0.000000 | 4.545286 | 1.820334 | 6.314735 |

| 4 | 2.602594 | 15.852312 | 14.182841 | 11.627708 | 0.730463 | 14.480029 | 10.971129 | 1.820334 | 21.325160 | 2.055642 | 14.182841 | 1.540963 | 12.510588 | 10.221051 | 0.730463 | 1.540963 | 1.194318 | 5.653921 | 1.194318 | 6.360100 |

X_train, X_test, y_train, y_test = train_test_split(X_reduced, y, test_size=0.2)

Linear Regression

# Instantiate model and create parameter grid

lr = linear_model.LinearRegression()

grid_params = {'fit_intercept': [True, False],

'normalize': [True, False],

'copy_X' : [True, False]}

# Instantiate new grid

grid = GridSearchCV(lr, grid_params, n_jobs=-1, cv=5)

# Linear Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 0.568 s

Best Accuracy Score:

0.8815714122815158

Best Parameters:

{'copy_X': True, 'fit_intercept': True, 'normalize': False}

# Instantiate and fit model with best parameters

lr = LinearRegression(fit_intercept=False, normalize=True, copy_X=True)

lr.fit(X_train, y_train)

y_pred = lr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(lr, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(lr.score(X_test, y_test)))

print('Cross Validation Scores:\n', scores)

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

91.45%

Cross Validation Scores:

[0.86964536 0.90312406 0.87734731 0.86610569 0.88772752]

Average Cross Validation Score:

88.08%

Root Mean Squared Error:

0.3011926609631838

KNN Regression

# Instantiate model and create parameter grid

knn = neighbors.KNeighborsRegressor()

grid_params = {'n_neighbors': list(range(1, 10)),

'weights': ['uniform', 'distance'],

'algorithm' : ['auto', 'ball_tree', 'kd_tree', 'brute']}

# Instantiate new grid

grid = GridSearchCV(knn, grid_params, n_jobs=-1, cv=5)

# KNN Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 4.46 s

Best Accuracy Score:

0.7573965453742735

Best Parameters:

{'algorithm': 'auto', 'n_neighbors': 7, 'weights': 'distance'}

# Instantiate and fit model with best parameters

knn = neighbors.KNeighborsRegressor(n_neighbors=7, weights='distance', algorithm='auto')

knn.fit(X_train, y_train)

y_pred = knn.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(knn, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(knn.score(X_test, y_test)))

print('Cross Validation Scores:\n', scores)

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

80.35%

Cross Validation Scores:

[0.7559988 0.81061274 0.72753457 0.75354858 0.73920998]

Average Cross Validation Score:

75.74%

Root Mean Squared Error:

0.4564285807903383

Random Forest Regression

# Instantiate model and create parameter grid

rfr = RandomForestRegressor()

grid_params = {'n_estimators': list(range(1, 10)),

'criterion': ['mse', 'mae'],

'max_depth': list(range(1, 10))}

# Instantiate new grid

grid = GridSearchCV(rfr, grid_params, n_jobs=-1, cv=5)

# KNN Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 70.4 s

Best Accuracy Score:

0.8517071234529742

Best Parameters:

{'criterion': 'mse', 'max_depth': 9, 'n_estimators': 8}

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/model_selection/_search.py:714: DataConversionWarning: A column-vector y was passed when a 1d array was expected. Please change the shape of y to (n_samples,), for example using ravel().

self.best_estimator_.fit(X, y, **fit_params)

# Instantiate and fit model with best parameters

rfr = RandomForestRegressor(n_estimators=9, criterion='mse', max_depth=8)

rfr.fit(X_train, y_train.values.ravel())

y_pred = rfr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(rfr, X_train, y_train.values.ravel(), cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(rfr.score(X_test, y_test.values.ravel())))

print('Cross Validation Scores:\n{}'.format(scores))

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

87.90%

Cross Validation Scores:

[0.84591098 0.86758539 0.85590976 0.82783851 0.84731086]

Average Cross Validation Score:

84.89%

Root Mean Squared Error:

0.3571122712911688

Ridge Regression

# Instantiate model and create parameter grid

rr = Ridge()

grid_params = {'alpha': [0.0001, 0.001, 0.01, 0.1, 1, 5, 10, 25, 50, 100],

'fit_intercept': [True, False],

'solver': ['cholesky', 'lsqr', 'sparse_cg']}

# 'solver': ['svd', 'cholesky', 'lsqr', 'sparse_cg', 'sag', 'saga']}

# Instantiate new grid

grid = GridSearchCV(rr, grid_params, n_jobs=-1, cv=5)

# Ridge Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 2.3 s

Best Accuracy Score:

0.8816035431498964

Best Parameters:

{'alpha': 0.01, 'fit_intercept': True, 'solver': 'cholesky'}

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/model_selection/_search.py:813: DeprecationWarning: The default of the `iid` parameter will change from True to False in version 0.22 and will be removed in 0.24. This will change numeric results when test-set sizes are unequal.

DeprecationWarning)

# Instantiate and fit model with best parameters

rr = Ridge(alpha=0.01, fit_intercept=True, solver='cholesky')

rr.fit(X_train, y_train)

y_pred = rr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(rr, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(rr.score(X_test, y_test)))

print('Cross Validation Scores:\n{}'.format(scores))

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

90.10%

Cross Validation Scores:

[0.90876598 0.91318546 0.89388285 0.88931054 0.8936684 ]

Average Cross Validation Score:

89.98%

Root Mean Squared Error:

0.3149498700624098

Lasso Regression

# Instantiate model and create parameter grid

lasso = Lasso()

grid_params = {'alpha': [0.0001, 0.001, 0.01, 0.1, 1, 5, 10, 25, 50, 100],

'fit_intercept': [True, False],

'max_iter': list(range(10))}

# 'solver': ['svd', 'cholesky', 'lsqr', 'sparse_cg', 'sag', 'saga']}

# Instantiate new grid

grid = GridSearchCV(lasso, grid_params, n_jobs=-1, cv=5)

# Ridge Regression

start = time.time()

grid.fit(X_train, y_train)

y_pred = grid.predict(X_test)

# Print results

print('Runtime for grid search: {0:.3} s'.format((time.time() - start)))

print('Best Accuracy Score: \n{}'.format(grid.best_score_))

print('Best Parameters: \n{}'.format(grid.best_params_))

Runtime for grid search: 8.92 s

Best Accuracy Score:

0.8717199839344799

Best Parameters:

{'alpha': 0.0001, 'fit_intercept': True, 'max_iter': 9}

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/model_selection/_search.py:813: DeprecationWarning: The default of the `iid` parameter will change from True to False in version 0.22 and will be removed in 0.24. This will change numeric results when test-set sizes are unequal.

DeprecationWarning)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.1345447112339042, tolerance: 0.0002292111729539456

positive)

# Instantiate and fit model with best parameters

lasso = Lasso(alpha=0.0001, fit_intercept=True, max_iter=9)

lasso.fit(X_train, y_train)

y_pred = rr.predict(X_test)

# Run cross validation and calculate RMSE

scores = cross_val_score(lasso, X_train, y_train, cv=5)

# Print results

print('Score With 20% Holdout:\n{0:.2%}'.format(rr.score(X_test, y_test)))

print('Cross Validation Scores:\n{}'.format(scores))

print('Average Cross Validation Score:\n{0:.2%}'.format(scores.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Score With 20% Holdout:

90.10%

Cross Validation Scores:

[0.90610849 0.89638496 0.88806663 0.87695657 0.88558265]

Average Cross Validation Score:

89.06%

Root Mean Squared Error:

0.3149498700624098

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.12588123641539328, tolerance: 0.000230805802977206

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10174824166285584, tolerance: 0.00018211493454537317

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10071330950203666, tolerance: 0.00018551750660764676

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.09815849040592911, tolerance: 0.00018381355085247963

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.10004544276933801, tolerance: 0.00018724225322712702

positive)

/Users/rakeshbhatia/anaconda/lib/python3.6/site-packages/sklearn/linear_model/coordinate_descent.py:475: ConvergenceWarning: Objective did not converge. You might want to increase the number of iterations. Duality gap: 0.0976469770913432, tolerance: 0.00018434117216229712

positive)

Our best model in this iteration was Linear Regression with an accuracy score of 91.45% and an RMSE of 0.30119.

Iteration 3 - PCA

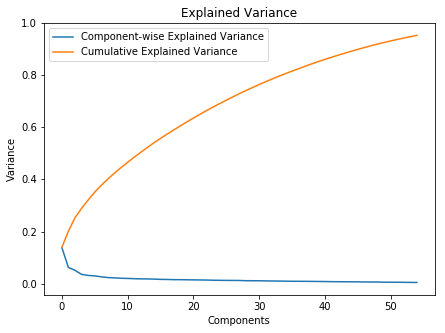

In this iteration, we will use PCA to reduce our feature set and then run the same five models again.

Train and Test PCA

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2)

# Standardize features

X_scaler = StandardScaler().fit_transform(X_train)

# Create PCA that retains 95% of variance

pca = PCA(n_components=0.95, whiten=True)

# Generate PCA

X_pca = pca.fit_transform(X_scaler)

# Print results

print('Original number of features:', X.shape[1])

print('Reduced number of features:', X_pca.shape[1])

Original number of features: 74

Reduced number of features: 55

fig = plt.figure(figsize=(7,5))

ax = plt.subplot(111)

ax.plot(range(X_pca.shape[1]), pca.explained_variance_ratio_, label='Component-wise Explained Variance')

ax.plot(range(X_pca.shape[1]), np.cumsum(pca.explained_variance_ratio_), label='Cumulative Explained Variance')

plt.title('Explained Variance')

plt.xlabel('Components')

plt.ylabel('Variance')

ax.legend()

plt.show()

Linear Regression

lr = linear_model.LinearRegression()

pipe = Pipeline([('pca', pca), ('linear', lr)])

pipe.fit(X_train, y_train)

y_pred = pipe.predict(X_test)

scores_train = cross_val_score(pipe, X_train, y_train, cv=5)

scores_test = cross_val_score(pipe, X_test, y_test, cv=5)

print('Cross Validation Scores - Training Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Training Set: \n{:.2%}'.format(scores_train.mean()))

print('\nCross Validation Scores - Test Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Test Set: \n{:.2%}'.format(scores_test.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Cross Validation Scores - Training Set:

[0.87208941 0.84418757 0.7806751 0.8441039 0.86005551]

Average Cross Validation Score - Training Set:

84.02%

Cross Validation Scores - Test Set:

[0.87208941 0.84418757 0.7806751 0.8441039 0.86005551]

Average Cross Validation Score - Test Set:

72.61%

Root Mean Squared Error:

0.4570210334553902

KNN Regression

knn = neighbors.KNeighborsRegressor(n_neighbors=7, weights='distance', algorithm='auto')

pipe = Pipeline([('pca', pca), ('knn', knn)])

pipe.fit(X_train, y_train)

y_pred = pipe.predict(X_test)

scores_train = cross_val_score(pipe, X_train, y_train, cv=5)

scores_test = cross_val_score(pipe, X_test, y_test, cv=5)

print('Cross Validation Scores - Training Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Training Set: \n{:.2%}'.format(scores_train.mean()))

print('\nCross Validation Scores - Test Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Test Set: \n{:.2%}'.format(scores_test.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Cross Validation Scores - Training Set:

[0.72190707 0.6670871 0.63802632 0.59866867 0.68857193]

Average Cross Validation Score - Training Set:

66.29%

Cross Validation Scores - Test Set:

[0.72190707 0.6670871 0.63802632 0.59866867 0.68857193]

Average Cross Validation Score - Test Set:

53.20%

Root Mean Squared Error:

0.608803837051414

Random Forest Regression

rfr = RandomForestRegressor(n_estimators=9, criterion='mse', max_depth=8)

pipe = Pipeline([('pca', pca), ('rfr', rfr)])

pipe.fit(X_train, y_train.values.ravel())

y_pred = pipe.predict(X_test)

scores_train = cross_val_score(pipe, X_train, y_train.values.ravel(), cv=5)

scores_test = cross_val_score(pipe, X_test, y_test.values.ravel(), cv=5)

print('Cross Validation Scores - Training Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Training Set: \n{:.2%}'.format(scores_train.mean()))

print('\nCross Validation Scores - Test Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Test Set: \n{:.2%}'.format(scores_test.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Cross Validation Scores - Training Set:

[0.77341358 0.69389058 0.67620675 0.70998848 0.77364554]

Average Cross Validation Score - Training Set:

72.54%

Cross Validation Scores - Test Set:

[0.77341358 0.69389058 0.67620675 0.70998848 0.77364554]

Average Cross Validation Score - Test Set:

59.05%

Root Mean Squared Error:

0.5319618143549292

Ridge Regression

rr = Ridge()

pipe = Pipeline([('pca', pca), ('ridge', rr)])

pipe.fit(X_train, y_train)

y_pred = pipe.predict(X_test)

scores_train = cross_val_score(pipe, X_train, y_train, cv=5)

scores_test = cross_val_score(pipe, X_test, y_test, cv=5)

print('Cross Validation Scores - Training Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Training Set: \n{:.2%}'.format(scores_train.mean()))

print('\nCross Validation Scores - Test Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Test Set: \n{:.2%}'.format(scores_test.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Cross Validation Scores - Training Set:

[0.8721049 0.84420952 0.78061565 0.84410179 0.86007169]

Average Cross Validation Score - Training Set:

84.02%

Cross Validation Scores - Test Set:

[0.8721049 0.84420952 0.78061565 0.84410179 0.86007169]

Average Cross Validation Score - Test Set:

72.65%

Root Mean Squared Error:

0.4570192792436453

Lasso Regression

lasso = Lasso(alpha=0.0001, fit_intercept=True, max_iter=9)

pipe = Pipeline([('pca', pca), ('lasso', lasso)])

pipe.fit(X_train, y_train)

y_pred = pipe.predict(X_test)

scores_train = cross_val_score(pipe, X_train, y_train, cv=5)

scores_test = cross_val_score(pipe, X_test, y_test, cv=5)

print('Cross Validation Scores - Training Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Training Set: \n{:.2%}'.format(scores_train.mean()))

print('\nCross Validation Scores - Test Set: \n{}'.format(scores_train))

print('\nAverage Cross Validation Score - Test Set: \n{:.2%}'.format(scores_test.mean()))

# Calculate root mean squared error

rmse = mean_squared_error(np.expm1(y_test), np.expm1(y_pred))**0.5

# Print result

print('Root Mean Squared Error:\n{}'.format(rmse))

Cross Validation Scores - Training Set:

[0.87197939 0.84464882 0.78050591 0.84374574 0.85970556]

Average Cross Validation Score - Training Set:

84.01%

Cross Validation Scores - Test Set:

[0.87197939 0.84464882 0.78050591 0.84374574 0.85970556]

Average Cross Validation Score - Test Set:

72.66%

Root Mean Squared Error:

0.45644992470380247

Our best model in this iteration was Lasso Regression with an average cross validation score (test set) of 72.66% and an RMSE of 0.45645.

Conclusion

Overall, the first two iterations appeared to provide the best results. There was even a slight improvement in some of the models from iteration 1 to iteration 2, when we limited the feature set to the 20 most important features. However, there was a significant drop-off when we used a PCA that retained 95% of the variance. Thus, utilizing the feature importances appears to be most optimal way to model this dataset.