Data Science Portfolio

DRILL: fixing assumptions

import math

import warnings

from IPython.display import display

from matplotlib import pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

from sklearn import linear_model

import statsmodels.formula.api as smf

from sklearn.preprocessing import StandardScaler

from sklearn.decomposition import PCA

# Display preferences.

%matplotlib inline

pd.options.display.float_format = '{:.3f}'.format

# Suppress annoying harmless error.

warnings.filterwarnings(

action="ignore",

module="scipy",

message="^internal gelsd"

)

Assumption one: linear relationship

# Acquire, load, and preview the data.

data = pd.read_csv('https://tf-curricula-prod.s3.amazonaws.com/data-science/Advertising.csv')

display(data.head())

# Instantiate and fit our model.

regr = linear_model.LinearRegression()

Y = data['Sales'].values.reshape(-1, 1)

X1 = data[['TV','Radio','Newspaper']]

# Create new squared features

data['TV^2'] = data['TV']**2

data['Radio^2'] = data['Radio']**2

data['Newspaper^2'] = data['Newspaper']**2

data['Sales^2'] = data['Sales']**2

X2 = data[['TV^2', 'Radio^2', 'Newspaper^2']]

regr.fit(X2, Y)

# Inspect the results.

print('\nCoefficients: \n', regr.coef_)

print('\nIntercept: \n', regr.intercept_)

print('\nR-squared:')

print(regr.score(X2, Y))

| Unnamed: 0 | TV | Radio | Newspaper | Sales | |

|---|---|---|---|---|---|

| 0 | 1 | 230.100 | 37.800 | 69.200 | 22.100 |

| 1 | 2 | 44.500 | 39.300 | 45.100 | 10.400 |

| 2 | 3 | 17.200 | 45.900 | 69.300 | 9.300 |

| 3 | 4 | 151.500 | 41.300 | 58.500 | 18.500 |

| 4 | 5 | 180.800 | 10.800 | 58.400 | 12.900 |

Coefficients:

[[ 1.42707531e-04 3.68654872e-03 -8.28260101e-05]]

Intercept:

[ 7.2029644]

R-squared:

0.799973684425

Assumption two: multivariate normality

Y = data['Sales'].values.reshape(-1, 1)

X = data[['TV', 'Radio', 'Newspaper']]

# Extract predicted values.

predicted = regr.predict(X).ravel()

actual = data['Sales']

# Calculate the error, also called the residual.

residual = actual - predicted

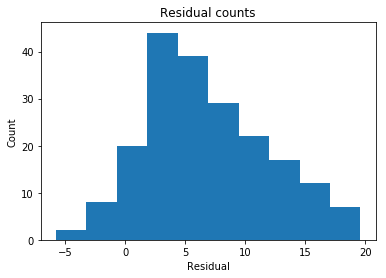

# This looks a bit concerning.

plt.hist(residual)

plt.title('Residual counts')

plt.xlabel('Residual')

plt.ylabel('Count')

plt.show()

Assumption three: homoscedasticity

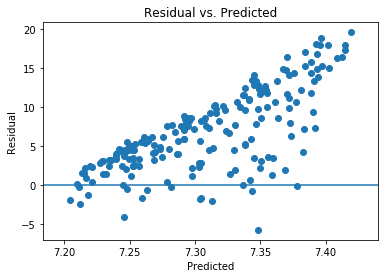

plt.scatter(predicted, residual)

plt.xlabel('Predicted')

plt.ylabel('Residual')

plt.axhline(y=0)

plt.title('Residual vs. Predicted')

plt.show()

Based on the scatter plot, it appears as though squaring the features improved the homoscedasticity.

Assumption four: low multicollinearity

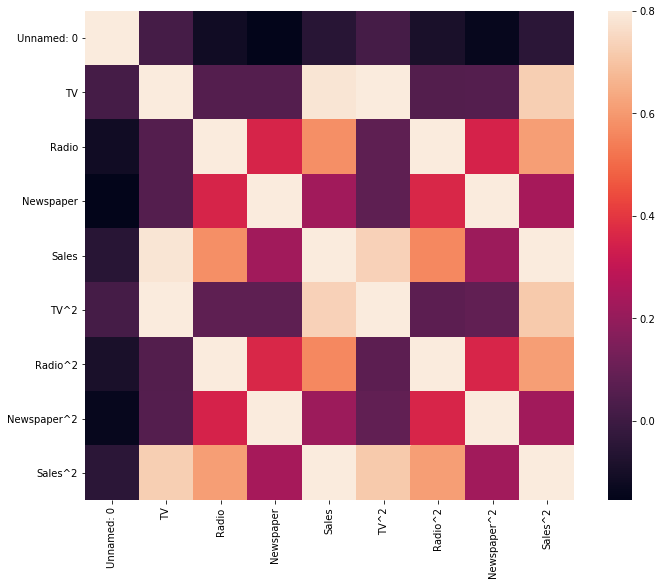

corrmat = data.corr()

f, ax = plt.subplots(figsize=(12, 9))

sns.heatmap(corrmat, vmax=.8, square=True)

plt.show()

display(data.corr())

| Unnamed: 0 | TV | Radio | Newspaper | Sales | TV^2 | Radio^2 | Newspaper^2 | Sales^2 | |

|---|---|---|---|---|---|---|---|---|---|

| Unnamed: 0 | 1.000 | 0.018 | -0.111 | -0.155 | -0.052 | 0.018 | -0.091 | -0.137 | -0.043 |

| TV | 0.018 | 1.000 | 0.055 | 0.057 | 0.782 | 0.968 | 0.051 | 0.056 | 0.729 |

| Radio | -0.111 | 0.055 | 1.000 | 0.354 | 0.576 | 0.079 | 0.967 | 0.352 | 0.610 |

| Newspaper | -0.155 | 0.057 | 0.354 | 1.000 | 0.228 | 0.076 | 0.361 | 0.940 | 0.238 |

| Sales | -0.052 | 0.782 | 0.576 | 0.228 | 1.000 | 0.736 | 0.562 | 0.216 | 0.980 |

| TV^2 | 0.018 | 0.968 | 0.079 | 0.076 | 0.736 | 1.000 | 0.075 | 0.085 | 0.715 |

| Radio^2 | -0.091 | 0.051 | 0.967 | 0.361 | 0.562 | 0.075 | 1.000 | 0.357 | 0.611 |

| Newspaper^2 | -0.137 | 0.056 | 0.352 | 0.940 | 0.216 | 0.085 | 0.357 | 1.000 | 0.228 |

| Sales^2 | -0.043 | 0.729 | 0.610 | 0.238 | 0.980 | 0.715 | 0.611 | 0.228 | 1.000 |

It appears that some of our features are highly correlated, particularly Radio/Sales and Newspaper/Sales.

correlation_matrix = data.corr()

display(correlation_matrix)

| Unnamed: 0 | TV | Radio | Newspaper | Sales | TV^2 | Radio^2 | Newspaper^2 | Sales^2 | |

|---|---|---|---|---|---|---|---|---|---|

| Unnamed: 0 | 1.000 | 0.018 | -0.111 | -0.155 | -0.052 | 0.018 | -0.091 | -0.137 | -0.043 |

| TV | 0.018 | 1.000 | 0.055 | 0.057 | 0.782 | 0.968 | 0.051 | 0.056 | 0.729 |

| Radio | -0.111 | 0.055 | 1.000 | 0.354 | 0.576 | 0.079 | 0.967 | 0.352 | 0.610 |

| Newspaper | -0.155 | 0.057 | 0.354 | 1.000 | 0.228 | 0.076 | 0.361 | 0.940 | 0.238 |

| Sales | -0.052 | 0.782 | 0.576 | 0.228 | 1.000 | 0.736 | 0.562 | 0.216 | 0.980 |

| TV^2 | 0.018 | 0.968 | 0.079 | 0.076 | 0.736 | 1.000 | 0.075 | 0.085 | 0.715 |

| Radio^2 | -0.091 | 0.051 | 0.967 | 0.361 | 0.562 | 0.075 | 1.000 | 0.357 | 0.611 |

| Newspaper^2 | -0.137 | 0.056 | 0.352 | 0.940 | 0.216 | 0.085 | 0.357 | 1.000 | 0.228 |

| Sales^2 | -0.043 | 0.729 | 0.610 | 0.238 | 0.980 | 0.715 | 0.611 | 0.228 | 1.000 |

features = ['TV', 'Radio', 'Newspaper', 'TV^2', 'Radio^2', 'Newspaper^2', 'Sales^2']

df_pca = data.loc[:, features].values

y = data.loc[:, ['Sales']].values

X = StandardScaler().fit_transform(df_pca)

Xt = X.T

Cx = np.cov(Xt)

print('Covariance Matrix:\n', Cx)

Covariance Matrix:

[[ 1.00502513 0.05508408 0.05693254 0.97252509 0.05109954 0.05590531

0.73256521]

[ 0.05508408 1.00502513 0.35588317 0.07903933 0.97160989 0.3541069

0.6134916 ]

[ 0.05693254 0.35588317 1.00502513 0.07682624 0.36322152 0.94439868

0.23939276]

[ 0.97252509 0.07903933 0.07682624 1.00502513 0.07509284 0.08590238

0.7185557 ]

[ 0.05109954 0.97160989 0.36322152 0.07509284 1.00502513 0.3583038

0.61367703]

[ 0.05590531 0.3541069 0.94439868 0.08590238 0.3583038 1.00502513

0.22896125]

[ 0.73256521 0.6134916 0.23939276 0.7185557 0.61367703 0.22896125

1.00502513]]

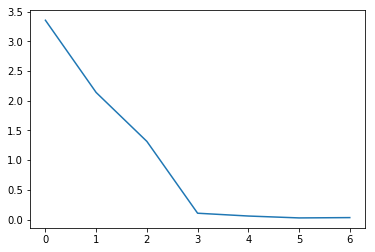

# Calculating eigenvalues and eigenvectors.

eig_val_cov, eig_vec_cov = np.linalg.eig(Cx)

# Inspecting the eigenvalues and eigenvectors.

for i in range(len(eig_val_cov)):

eigvec_cov = eig_vec_cov[:, i].reshape(1, 7).T

print('Eigenvector {}: \n{}'.format(i + 1, eigvec_cov))

print('Eigenvalue {}: {}'.format(i + 1, eig_val_cov[i]))

print(40 * '-')

print(

'The percentage of total variance in the dataset explained by each',

'component calculated by hand.\n',

eig_val_cov / sum(eig_val_cov)

)

Eigenvector 1:

[[-0.32192638]

[-0.41441704]

[-0.32480276]

[-0.33074094]

[-0.41479104]

[-0.32324108]

[-0.48290695]]

Eigenvalue 1: 3.3533907440501256

----------------------------------------

Eigenvector 2:

[[-0.53183042]

[ 0.26803955]

[ 0.35554971]

[-0.51574108]

[ 0.27193793]

[ 0.35385085]

[-0.23183203]]

Eigenvalue 2: 2.138315141603013

----------------------------------------

Eigenvector 3:

[[ 0.16157412]

[-0.4372079 ]

[ 0.51608197]

[ 0.16734606]

[-0.43358999]

[ 0.52089634]

[-0.17048307]]

Eigenvalue 3: 1.3152329266320908

----------------------------------------

Eigenvector 4:

[[ 0.13700407]

[ 0.2664073 ]

[-0.13288173]

[ 0.44772813]

[ 0.22523894]

[ 0.09618972]

[-0.7950811 ]]

Eigenvalue 4: 0.10705708130779526

----------------------------------------

Eigenvector 5:

[[ 0.10729353]

[ 0.01308928]

[ 0.69087275]

[ 0.00494538]

[ 0.07675588]

[-0.69424467]

[-0.15205271]]

Eigenvalue 5: 0.05981778381043827

----------------------------------------

Eigenvector 6:

[[-0.74294797]

[ 0.01158729]

[ 0.07664522]

[ 0.62498504]

[-0.12455246]

[-0.08476171]

[ 0.16945618]]

Eigenvalue 6: 0.02803879045367865

----------------------------------------

Eigenvector 7:

[[-0.07183251]

[-0.70284004]

[-0.03016256]

[ 0.07433458]

[ 0.7027521 ]

[ 0.02364543]

[ 0.00096626]]

Eigenvalue 7: 0.033323411539842196

----------------------------------------

The percentage of total variance in the dataset explained by each component calculated by hand.

[ 0.47666054 0.30394622 0.18695097 0.0152174 0.00850267 0.00398551

0.00473668]

plt.plot(eig_val_cov)

plt.show()

It turns out that doing PCA indicates that we should get rid of the extra squared features. Only the first three features (TV, Radio, Newspaper) have eigenvalues greater than 1. Approximately 96% of the variance is captured in these three features.